Silicon Carbide Power Semiconductors Market Overview:

The global silicon carbide power semiconductors market size was valued at $302 million in 2017 and is projected to reach $1,109 million by 2025, registering a CAGR of 18.1% from 2018 to 2025. In 2017, the Asia-Pacific region constituted the highest share in the global silicon carbide power semiconductors market. This region is expected to grow at the fastest rate during the forecast period.

Silicon carbide is a semiconductor developed by the combination of silicon and carbon. It exhibits a level of hardness that is approximately equivalent to a diamond, which enables SiC semiconductors to operate in extreme conditions. Moreover, characteristics of silicon carbide such as higher breakdown electric field strength, wider band gap, lower thermal expansion, and resistance to chemical reaction, enable it to gain an edge over traditional silicon semiconductors in the power semiconductors market. The energy required by silicon carbide electrons to jump from the valence band to the conduction band is three times to that of the silicon power semiconductor. This property enables SiC-based electronic devices to withstand higher voltages and temperatures than their silicon counterparts. Furthermore, they carry much higher current, i.e., almost five times that of their silicon counterparts; therefore, they offer lower switching loss and lower ON resistance, which results in lower power loss.

Growing demand for power electronics that drives the growth of the SiC power devices market. Power electronics ensures control and conversion of electrical power effectively and efficiently. Increasing demand for power electronics across various industry verticals, such as aerospace, medical, and defense, plays a crucial role in increasing the adoption of SiC power devices. Moreover, growing demand for SiC-based photovoltaic cells in developing countries, including China, Brazil, and India, fuels the growth of SiC-based power semiconductors. One of the major restraints associated with this market is the huge wafer cost required for producing silicon carbide-based semiconductors. Moreover, challenges associated with designing of SiC MOSFETs are impediments in the production of SiC power semiconductors.

On the other hand, increase in the number of modern applications requiring SiC power devices offers lucrative opportunities for the market. In the automotive sector, traction inverters in electric vehicles are subjected to high thermal and load cycling. SiC has increased reliability and higher efficiency, ability to operate at higher temperatures, reduced size, and higher voltage capabilities, which make it ideal for application in the electric vehicle industry.

The key players operating in the Silicon Carbide Power Semiconductors Market are Infineon Technologies AG, Microsemi Corporation, General Electric, Power Integrations, Toshiba Corporation, Fairchild Semiconductor, STMicroelectronics, NXP Semiconductors, Tokyo Electron Limited, Renesas Electronics Corporation, ROHM, and Cree, Inc.

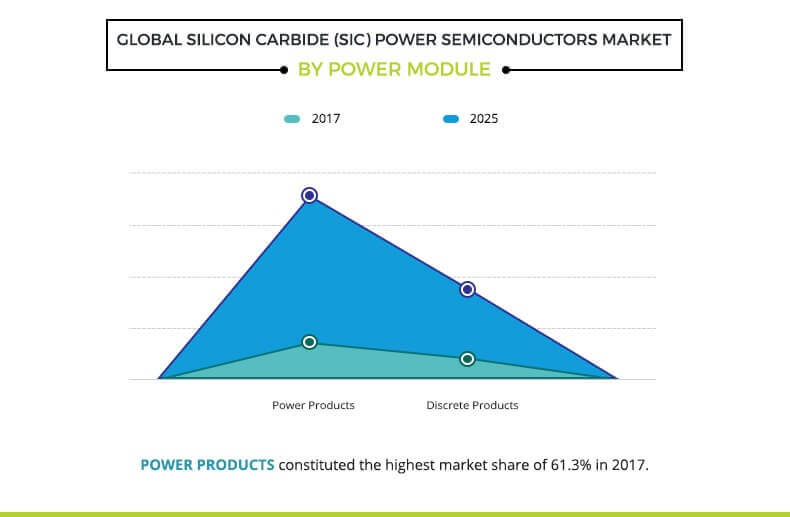

On the basis of power module, the power product segment occupied the highest market share of 61.2% in 2017. According to industry vertical, use of silicon carbide power modules is expected to grow at the fastest CAGR of 20.5% in the automotive sector during the forecast period.

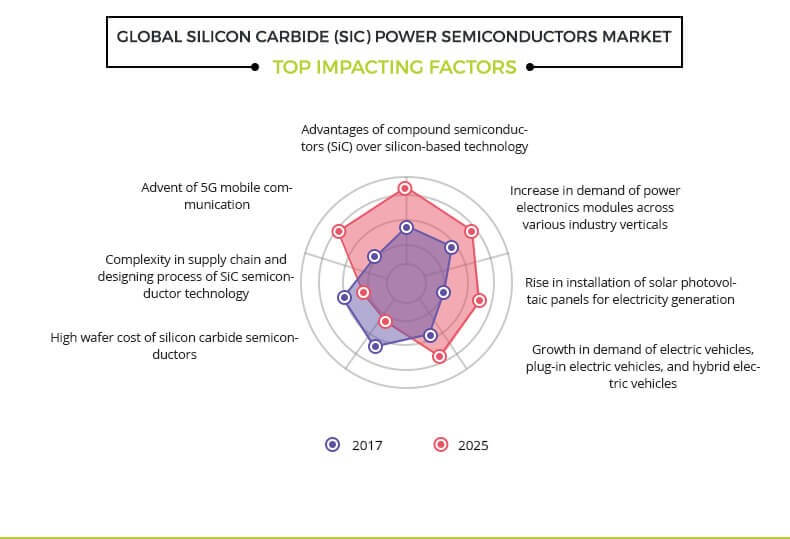

Top Impacting Factors

Advantages of Compound Semiconductors (SiC) Over Silicon-based Technology

The electronic properties of silicon carbide power semiconductors are superior to those of silicon. They possess higher saturated electron velocity, and electron mobility. SiC power semiconductors are comparatively less affected by overheating, owing to their wider energy bandgap. They also tend to create lesser noise in electronic circuits than silicon devices, thus resulting in minimized power loss. These enhanced properties stimulate increased usage of compound semiconductors, such as SiC power devices, in satellite communications, mobile phones, microwave links, and high-frequency radar systems. Thus, this superiority of silicon carbide power semiconductors over silicon drives the market growth.

Increase in Demand of Power Electronics Modules Across Various Industry Verticals

Power electronics is the branch of electronics that deals with the control and conversion of electrical power. The characteristics of silicon carbide semiconductors, such as higher breakdown electric field strength and wider band gap, enable their usage in power electronics; for instance, these devices play an extremely crucial role in controlling automotive electronics such as electric power steering, hydro electric vehicles main inverter, seat control, braking system, and others. SiC power electronics also facilitates energy conversion in generators and actuators integrated in aircrafts. Along with automotive and aircraft, the growth of power electronics is driven by its increasing usage in several applications such as industrial motor drives, electric grid stabilization, and consumer electronics. Therefore, its effective power control and management feature for industrial operations or functioning of electrical/electronic devices makes it suitable for different industry verticals.

High Wafer Cost of Silicon Carbide Semiconductors

The major impediment in the production of SiC-based power devices is the high wafer cost. The price of SiC semiconductors is higher than the silicon semiconductors that they have been aiming to replace. High-purity SiC powder and high-purity silane (SiH4) are the critical precursors for producing SiC layers in the chips. High-purity SiC powder is currently available from a limited number of suppliers and is relatively expensive. Bridgestone (United States), Washington Mills (United States), LGInnotek (Korea), and Pallidus (United States) are the few companies involved in manufacture of high-purity SiC materials, while high-purity silane is produced by a few large multinational industrial gas companies. The fewer suppliers of these raw materials required in the manufacturing of silicon carbide wafers have resulted in their higher cost. In addition, major companies, such as Cree, Inc. and Dow Corning that are majorly involved in the production of semiconductor devices, provide SiC wafers and substrates. This has resulted in the consolidation of the market. Hence, higher bargaining power of silicon carbide wafer suppliers hampers large-scale adoption of silicon carbide wafers.

Advent of 5G Mobile Communication

The huge dependency on digital infrastructure has been driving the research & development of high-speed internet. 5G, that is, 5th generation wireless mobile standard is expected to be deployed till 2020 across various developed and developing nations such as the U.S., China, and India. This wireless standard is expected to offer explosive data transfer speed up to 10 Gbps. This infrastructure is expected to support the rising penetration of internet of things and smart devices, which require high data transfer speed for efficient performance. The mobile communications create the requirement for power semiconductors, particularly the radio frequency (RF) type. Several power amplifiers are expected to be installed at each base station, owing to the proliferation of numerous 5G base stations. Silicon carbide (SiC), gallium arsenide (GaA), and gallium nitride (GaN) are among the few compound semiconductors currently considered to be used in the production of power semiconductors for the fifth-generation communication. Ultimately, it is expected to provide enormous opportunity for the vendors during the forecast period.

Key Benefits for Stakeholders

- This study comprises the analytical depiction of the global silicon carbide (SiC) power semiconductors market analysis along with the current trends and future estimations to depict the imminent investment pockets.

- The overall SiC power semiconductor market potential is determined to understand the profitable trends to gain a stronger foothold.

- The report presents information related to the key drivers, restraints, and opportunities of the global silicon carbide (SiC) power semiconductors market with a detailed impact analyses.

- The current market is quantitatively analyzed from 2018 to 2025 to benchmark the financial competency.

- Porters Five Forces analysis illustrates the potency of the buyers and suppliers in the industry.

Silicon Carbide Power Semiconductors Market Report Highlights

| Aspects | Details |

| By Power Module |

|

| By Industry Vertical |

|

| By Region |

|

| Key Market Players | POWER INTEGRATION, INC., NXP SEMICONDUCTORS, ROHM CORPORATION, TOSHIBA CORPORATION, FAIRCHILD SEMICONDUCTOR (ON SEMICONDUCTOR), MICROSEMI CORPORATION, GENERAL ELECTRIC COMPANY, CREE, INC., TOKYO ELECTRON LIMITED, RENESAS ELECTRONICS CORPORATION, STMICROELECTRONICS, INFINEON TECHNOLOGY |

Analyst Review

Silicon carbide (SiC) power semiconductor is a power device, which is used to control the distribution of power in an electronics system. Silicon carbide power semiconductors play a vital role in the power semiconductors market. The wider band gap, high switching frequency, and high electric field strength of SiC power devices allow them to be operated at higher temperatures and volumes as compared to their silicon counterparts. The silicon carbide power devices market has witnessed significant growth, owing to increasing number of industrial sectors that require SiC power devices, such as telecom, manufacturing, automotive, and energy & power sectors.

Increasing usage of efficient power electronics systems in IT & telecommunications, electric and hybrid electric vehicles, renewable energy systems such as solar and wind energy systems, and industrial motor drives significantly impacts the growth of the silicon carbide power semiconductors market. However, high cost of silicon wafers, which are used for the manufacturing of SiC-based power devices, restrains the growth of the market.

On the basis of power module, the power product segment accounted for the highest revenue in the market in 2017, because of its smaller solution size as compared to discrete products. Owing to the increasing penetration of electric vehicles, the use of silicon carbide power semiconductors is expected to grow the fastest in the automotive sector during the forecast period.

Among the analyzed geographical regions, the Asia-Pacific is expected to account for the highest revenue in the global market throughout the forecast period (2018–2025), followed by Europe, North America, and LAMEA. Moreover, the Asia-Pacific is expected to witness the highest growth rate, owing to the increasing usage of power electronics in developed countries, such as China, South Korea, and Japan, which indicate lucrative prospects for silicon carbide power semiconductor providers in the Asia-Pacific region.

Loading Table Of Content...